How Should A Beginner Start A Budget?

One of the most critical components of our life is budgeting. Whether you’re making a personal budget to keep your finances in order or working with a large accounting company on a national or global scale, your budget may affect every action or choice you make. As a result, it’s critical to have a solid, well-thought-out budget.

A monthly budget will keep you organized and focused on your particular financial objectives on a personal level. It may sound scary if you’ve never made or managed a budget before, but it doesn’t have to be. These methods will assist you in creating a budget and, as a result, become more organized.

Calculate Your Earnings

You must first determine how much money you have to deal with before you can begin budgeting.

Begin by making a list of all of your sources of income, including rental income and money earned from a side job. It’s possible that your monthly income is merely what you bring home from work. If your earnings aren’t always steady — for example, if you work a variable amount of hours each week as a freelancer – average your earnings over the preceding three months and use it as a baseline.

If you want to save money and do it playfully, you should try the 100 envelope challenge. Crossing out empty cells with the amount of deferred savings can be a really exciting and motivating activity for you.

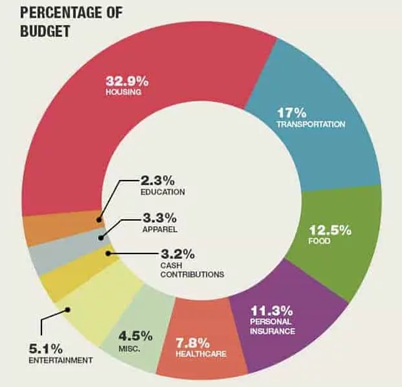

Make a List of All Of Your Monthly Costs

It’s time to look at your monthly costs now that you’ve calculated your monthly revenue. Begin by listing all of your fixed costs, which are the monthly bills that you must pay, such as student loan payments, Internet, food, petrol, auto payments, insurance, utility bills, and rent.

If the prices for any of these items tend to fluctuate, calculate the average price for the last three months and use that number. A free household budget worksheet can help you with this.

You can discover your overall monthly financial commitments by adding up the prices of your fixed expenses. Subtract this amount from your monthly earnings. This will show you how much money you have left over each month for personal objectives and discretionary expenditures.

Make a List of Your Financial Objectives

The next step is to determine your financial objectives. This is critical because it allows you to create a strategy that prioritizes your priorities.

Getting out of debt, saving for a down payment on a home, paying off your automobile, and preparing for retirement are all examples of financial objectives. Consider your own financial objectives and create some objectives with a free monthly budget template.

When creating a short-term or long-term budget plan, listing your objectives might help you keep perspective and prioritize your expenditures. It is natural that you will want to calculate more detailed statistical information.

Make a List of Your Discretionary Spending

Make a List of Your Discretionary Spending

Life is more than simply paying bills and putting money aside. Take into consideration your discretionary spending – the money you spend on items you don’t really need.

Going out to dine, giving presents, taking trips, buying new clothing, and seeing movies or performances are just a few examples. Some expenses, such as monthly entertainment or subscription services, may be considered discretionary expenditures.

How much money do you have left over in your budget after you’ve paid your bills and set aside money for your long-term financial goals? This is the amount of money you have set aside for amusement and other non-essential expenses.

Make sure to keep these expenses to a minimum depending on your financial situation. Discretionary spending comes after fixed monthly expenses for a reason: it’s critical to pay off debts and cover essential expenses before taking a trip or purchasing a new television.

To Establish a Complete Budget, Subtract Your Total Costs from Your Profits

So far, you’ve got a sense of how each area of your budget — monthly commitments, discretionary spending, and financial objectives — appears. Now is the time to complete the image. Subtract your total monthly expenses from your monthly income after adding up all three categories.

If the answer is positive, it indicates that you are taking in more money than you are spending. If that’s the case, then kudos to you; you’ve got a surplus. You may either save this money or spend it to supplement your other expenses. You might, for example, make a lump-sum payment on your student debts using budgeting worksheets for students or put the money into a vacation fund.

You have just enough money but a little margin for error if you come up with a figure close to zero. This might be a concern if anything unexpected occurs. Consider tweaking your budget or finding methods to reduce your monthly expenses to offer yourself some breathing space in this instance.

If you obtain a negative result, it’s time to look at your budget again: you’re spending more than you make. The most effective strategy to change your budget is to reduce the amount you spend each month on non-essential items. When creating and managing a monthly budget, needs should always come first.

Keep an Eye on Your Budget And Make Adjustments As Needed

Maintain a constant eye on your budget and make any required adjustments along the road; you never know when an unforeseen incident may arise that will alter your financial condition. It’s a good idea to sit down with your significant other on a monthly (or even weekly) basis to review and discuss your personal financial objectives for the following month.

If you’re just getting started and have never set and kept a monthly budget, you’re not alone in thinking it’s difficult. The first few months may be difficult, but they will set you on the path to a much better, more structured, and happier financial state.